Q3 2023 - State of Venture Update

Return of the Old Normal

Taking inspiration from my portfolio companies which send wonderful updates, I decided to put pen to paper on a quarterly basis to outline my current thoughts on the venture fundraising environment. My initial thought was to only send this internally, but I decided to publish a delayed and (slightly) redacted version of what I send my portfolio. The intent is to cover where I see the fundraising market + the broader macro picture + other musings on startups. It’s important to note that these are my views, not the fund’s views. None of what I mention should be construed as investment advice — make your own decisions!

Fundraising market -- return to the old normal

In software, we're starting to see more activity in the early-stage, but late-stage remains quiet outside of a few exceptional companies. Seed has been quite active this quarter with YC in August and my impression is a lot of those companies got a great reception. I've started to hear about more Series As getting done (at 2018 prices), although we haven't been too active ourselves (not for lack of interest though, we are open for business). The late-stage remains a desert. From anecdotes, my good friend at a Top-Tier Growth Fund says they've only done 2 deals in the last 27 months. I don't think this is for a lack of capital in the market, but instead a mismatch of valuation expectations. Instacart seems poised to price ~76% down from their last mark (back to the 2018 price) in the IPO and I think a lot of late-stage companies will be in this spot. It's a lot easier to take this haircut in the public markets where the pref gets wiped, vs. doing so in the private markets. I think this pref dynamic will drive more IPOs next year.

In Bio, we see the opposite. Early-stage funding is relatively quiet/challenging, and the late-stage market is more active -- with the caveat that it remains very difficult to get external capital unless you are clinical, or funding through clinical readouts. The "next round" in Bio is not a given, so investors want to see their round of funding get through unquestionable value-drivers (i.e. human readouts where possible).

Broadly data seems to show we may be near a bottom in capital deployment:

Source: SVB State of the Markets H2 2023

The dominant narrative I see around SV is that valuations/the venture markets are "depressed" and companies/commentators are encouraging companies to survive until conditions improve. I think this type of narrative -- implying the current environment is an aberration -- belies the fact that the present environment is much more normal than was 2021. In my view, the present environment is the new normal, and the new normal looks a lot like the old normal of 2018.

Why do I think this? Because in many ways public market valuations/expectations are optimistic/aggressive, and public software multiples have rallied back to more normal levels.

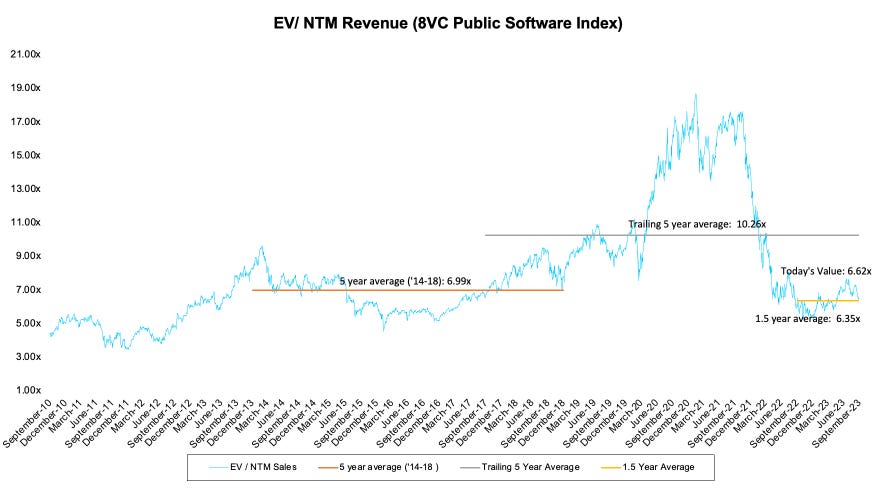

If we dissect the data, public software multiples have rallied back from the bottom, back to the mid-2010s average. It looks much more like '14-’18 which is in reality a pretty average environment for Software Multiples.

Source: Capital IQ, Company Filings, 8VC Estimates

Commentary: Public market SaaS multiples are down 33% from the 5-year average, but near the 5-year average of ‘14'-'18

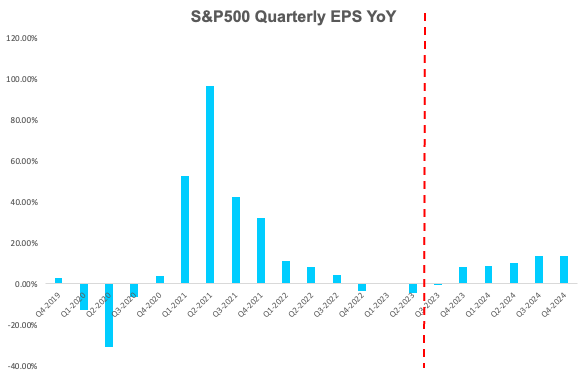

This is all in the face of positive economic data and aggressive earnings (forward PE ratios near 20x -- very high). Will there be a recession? Basically no, at least when you look at corporate earnings. The expectation is that earnings have bottomed in Q3 and will start growing again. No recession here.

Source: IBES Refinitiv, Company Reports, S&P Dow Jones

Commentary: S&P 500 earnings are expected to increase over the next 5 quarters. The market is pricing in fairly optimistic growth — not a recession or slowdown!

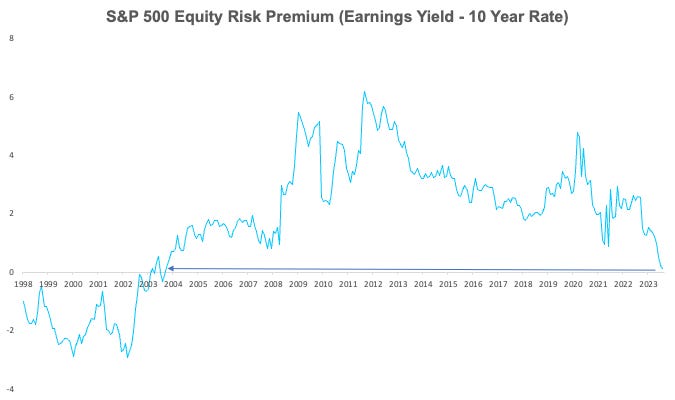

Examining the broader market, valuations indicate that the S&P is priced quite aggressively. Instead of using P/E ratios, I prefer to consider the Equity Risk Premium (defined as the yield of equities minus the risk-free rate). This metric excels over P/E ratios in normalizing valuations in the context of interest rates. By this standard, the broader market is as expensive as it was prior to the Global Financial Crisis (GFC). This certainly doesn't suggest things are depressed!

Source: S&P Down Jones, Company Reports, FRED

Commentary: The Equity Risk Premium (ERP) represents the amount of risk priced into equities. A low ERP indicates that stocks are expensive relative to the risk-free yield, typically measured using the 10-year rate. Based on this metric, stocks are currently more expensive than they have been at any point in the past two decades.

What's all this mean? It means a lot of positive news has been factored into financial markets, and the present venture environment stands in the presence of an aggressive market backdrop. We shouldn't expect significant improvements in the venture funding markets from their current state. Everyone should plan accordingly; capital is expensive and your growth needs to be efficient. This was the way of the past, and it's likely to remain so in the future. The old normal is maybe not as fun but it is the way.

What does the old normal look like? If you're a post-seed software company, assume you're going to get 10x 6- to 12- months out ARR if your growth is efficient (good growth rate, burn ratio and magic number). If you're a bio company, you won't be able to fund long platform builds anymore. Your first round needs to get you to an IND, and your subsequent rounds need to get through clinical readouts.

Inflation

A counterargument to my perspective on the 'old normal' is that a Fed Pivot is imminent, which would result in lower rates and another liquidity-driven surge. I think that's very unlikely anytime soon for a few reasons. First, by the numbers, Core CPI was 4.7% in July. This is very high and well above target. We are not close to normalizing inflation.

Second, the Fed is cognizant of the fact that inflation can be very volatile, and unlike the '70s they will be loath to lower rates or step off the gas unless inflation materially abates and unemployment increases (aside: if they forget this fact, inflation will probably come back and force them to raise again anyway). Compare inflation from the '70s to today to appreciate the volatility of high-inflation environments.

Source: Bloomberg

Commentary: The graphic juxtaposes inflation from the past decade with inflation from 1966 to 1982. Although the exact scales might not be directly comparable, the aim is to illustrate that during periods of high inflation, inflation can be extremely volatile and challenging to control. The Fed is cognizant of this history and is likely to maintain higher interest rates to avoid a recurrence of the inflation spike seen from 1978 to 1982. It’s unlikely we will see another liquidity boom like we did in 2020/2021.

Third, most macro drivers point to high inflation. Unemployment remains very low. Most debt in the US is fixed rate (this differs from other countries) and so the effect of interest rate increases has not been felt outside of core cyclicals. The fiscal situation in the US is abysmal, we are running war-time deficits which are stimulating the economy while the Fed is trying to slow the economy. And to make matters worse, the government is one of the only entities that issues a majority of short-term debt, so it is feeling interest rate hikes in the deficit. Lastly, I think the conflict in Ukraine is likely to make energy and soft-commodity markets much more volatile this winter. All of this is inflationary!

AI

The lone bubble spot we've seen in the market has been Generative AI. I'll delve into my AI thesis in the next update, but I genuinely believe that the impact of this new generation of models will be revolutionary over the next decade. It will transform how every industry operates. We continue to see many companies raising incredible amounts of capital at irrational valuations with relative ease, particularly for foundation models and AI infrastructure.

I believe the majority of the capital invested today will be lost, similar to what happened in the .com era. However, I expect there will be a select group of companies that endure and build the future. One theory I hold is that market cycles now move faster than in the past due to the rapid dissemination of information. I predict the AI bubble will burst sooner than the .com bubble did (1995-2000) -- to be succeeded by a long bull market for Generative AI. It might not happen immediately, but we are already witnessing a gradual waning of interest in Generative AI from peak. Data from SimilarWeb on GenAI traffic shows there are declines across the board (and it’s widely reported ChatGPT revenue slowed in the summer) . I believe that a drop in interest would be beneficial for the sector. [I can’t share this traffic data publicly since it is copyrighted]

Our present interest is heavily concentrated in AI-enabled services. I think the next wave of Vertical Software is AI-enabled services automation. If you know of any labor/services-heavy parts of your vertical market, please send me a note about it.

Conclusion

My note is not meant to be pessimistic but sobering. There is no depression in capital markets, but rather a return to the old normal. Great businesses can be built in any market environment, and in particular, exceptional businesses thrive in loose labor markets. In this note, I haven't made many forward-looking statements, I'll save forward-looking predictions for the next note. But I tend to think most risks in the market remain to the downside. Conditions are likely to get worse than better since we're priced to perfection. It's important, however, to know that great businesses will always endure and can raise capital in any environment -- the correct takeaway is to adjust expectations.

What makes me bullish?

Bad companies are being washed out and good companies are finding more talent available. A company I'm on the board of had 200 applications for a Sr Engineering role in a week! This rings true for our bio companies as well.

What makes me nervous?

Most companies are still missing projections, and it seems *hard* to sell software. This makes me think the real economy is weaker than employment and S&P multiples imply.

Until next time.

Good things I've read/listened to this quarter: