Q4 2023 - State of Venture Update & 2024 Outlook

80% Growth is the New 200%

I hope everyone had a restful holiday season, despite the somewhat lackluster end to 2023 in the private markets. I'd confidently say that the dominant theme of the year, unsurprisingly, has been the ascendance of AI in the innovation economy. In many ways, I believe the AI wave will be a savior for the technology market. This year, AI significantly contributed to the outperformance in the equity markets, with the majority of outsized returns coming from the 'Magnificent 7' companies, each deeply involved in AI. Additionally, AI is playing a pivotal role in revitalizing the Venture Capital market. As opportunity in cloud, social, mobile, AR, and BioTech ventures wane, the AI wave is becoming increasingly dominant.

Fortunately for most mega-funds, the extreme capital inefficiency of foundational AI infrastructure companies aligns well with their business need to deploy mega-funds biennially. It's a true match made in heaven! We'll see if such a strategy yields expected returns. I remain a bit skeptical and generally bullish on model bifurcation: OpenAI for high-complexity use-cases, Open Source for mid-range applications, and little in between.

Venture Staffing

To me, the real story of this quarter is not so much about the market for deals in Venture Capital (VC), but rather about the market for people. My view is that we are likely to witness a significant exodus and shrinking of VC firms over the next 2-3 years. I've expressed this perspective in a well-timed tweet recently:

My tweet preceded/was coincident with a few big departures that got announced:

And there are several other unannounced departures I won't disclose here, but I can share if you're curious. I believe this is a trend we'll see over the next few years for a few reasons:

Performance: As we emerge from the shadow of 2021, we are likely to witness significant portfolio losses, potentially leading to the end of many careers. A mentor of mine once said, 'The remedy to an excess capital environment is that capital gets destroyed' (h/t Patrick Kenary). Consequently, following the excesses of 2021, numerous careers may also come to an end.

Shrinking Dealflow/Market: We are witnessing the culmination of several technology waves: mobile, social, and cloud. These sectors have experienced a secular decline over many years. This trend seemed to reverse temporarily with Tiger's influx of liquidity in 2021, but this only created a false sense of vitality in the innovation economy. While BioTech hasn’t been declining secularly, it has certainly peaked after the 2020 sugar-rush and is now undergoing significant retrenchment in company formation as well. Currently, Artificial Intelligence is emerging as the new trend, rejuvenating the market. Despite the AI renaissance, I estimate that the opportunity for venture investment is still about 60-70% smaller than during the 2018-2021 period, which implies a reduced need for VCs.

Beginning of Cycle dynamics: The 10-year technology bull market has ended, reaching its zenith in 2021. Many VCs made significant profits and, frankly, lack the will or desire to engage in another decade-long cycle at the start of the new bull market. The AI wave will build a new generation of fortunes, but as always, it will be a messy, hard, competitive process, requiring 'hand-to-hand combat' with limited immediate rewards. For some, the drive to continue will wane – after all, life is finite.

Personally, I'm in the grindset. I'm fully committed and eager to tackle the challenges of transitioning from one supercycle to the next, embracing both the challenging ending and optimistic beginning it brings.

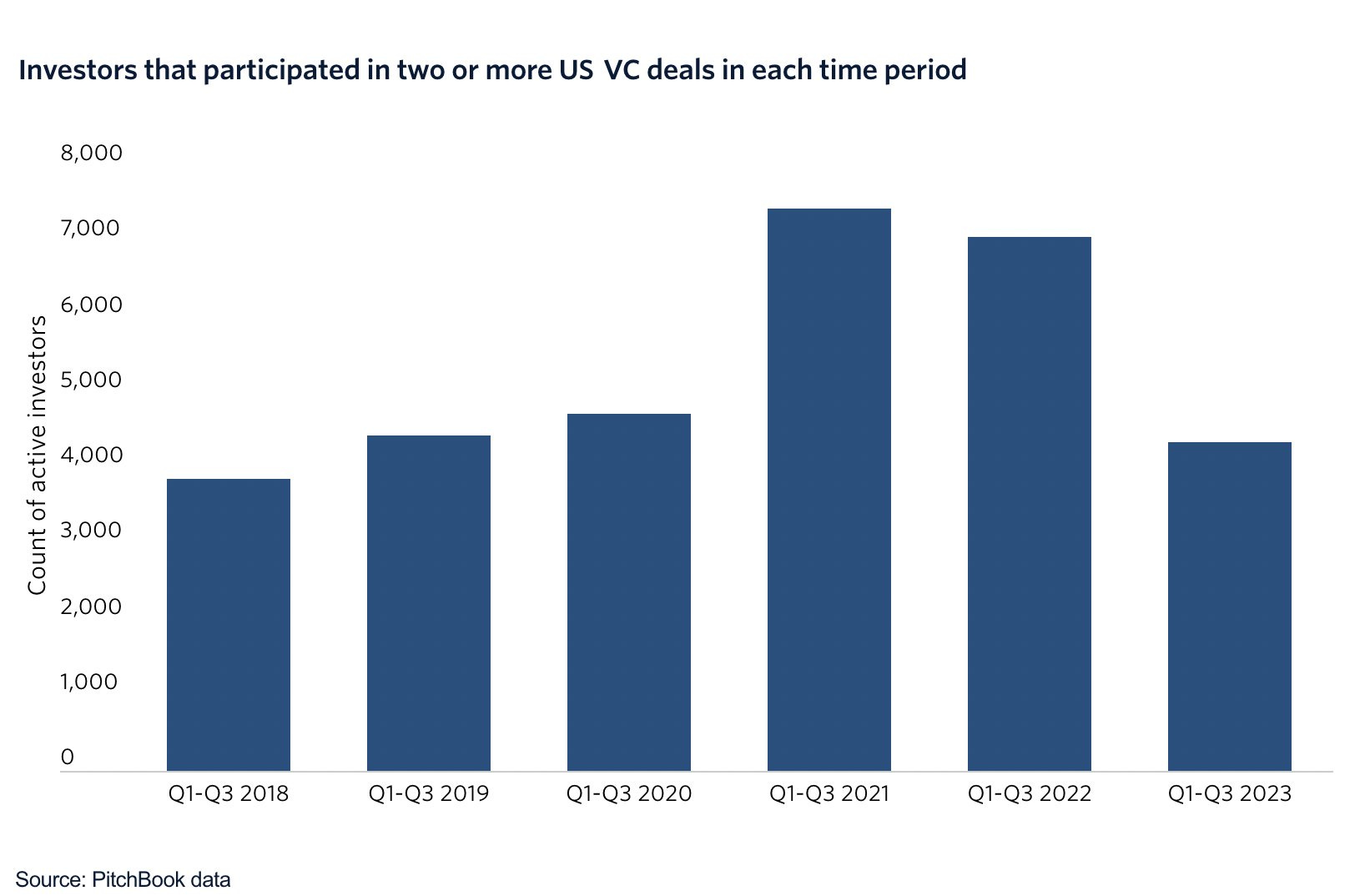

According to PitchBook data, the trend of reduced VC staffing appears to be underway. I wouldn't be surprised if, within the next 1-2 years, we see numbers falling below those of 2018

The number of investors engaged in deal-making has decreased by 38%, a trend distinct from the 72% reduction in funds raised this year. This fund decline is more a result of lower deployment rates rather than a decrease in the number of investors.

Fundraising Market

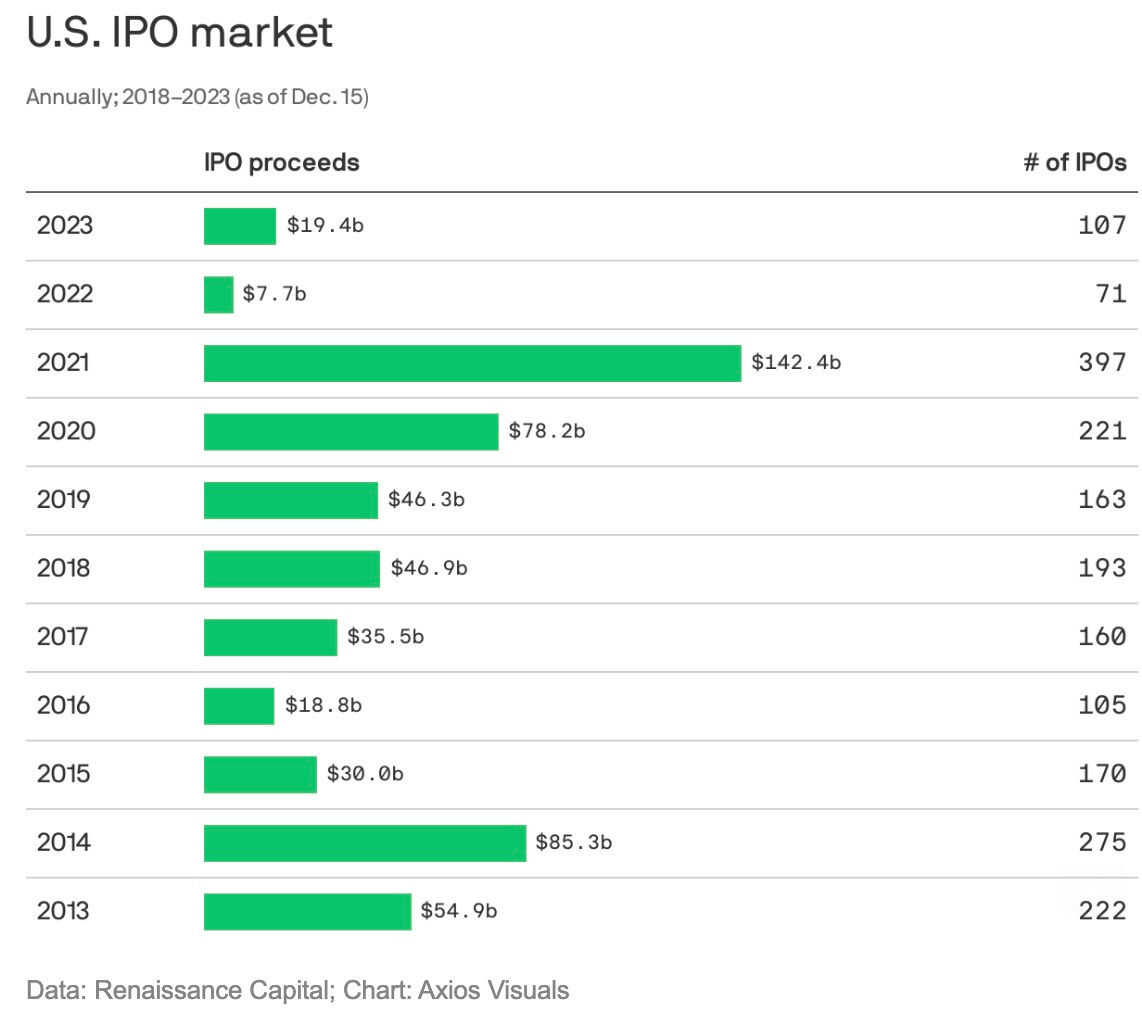

Overall, this quarter, public market software multiples have slightly increased, based on the 8VC Public Software Index. This mirrors what we've seen in the private early-stage market since last quarter as well. The growth market has continued to be subdued, not helped by the mixed IPO performance of the three major Q4 IPOs.

By the numbers, 2023 in fact has remained a fairly quiet IPO year, well below-trend:

But I believe that this scenario is set to change. In 2024, I anticipate that more companies will recognize public markets as a credible path for raising capital. This could circumvent the challenges associated with structured financings or down rounds in the private markets. An IPO leads to an automatic conversion to common stock, which clears out the preference stack and simplifies a company's financial structure. Additionally, it necessitates improved governance, which could be leveraged as a quid pro quo for approving a down-round IPO.

While there is a prevailing 'wisdom' among bankers and pundits that 'the IPO window is closed,' I have always considered this perspective to be rather simplistic. Various excuses are often cited, such as 'not enough analysts,' 'banks won't build the book,' or 'the last few IPOs didn't pop.' However, in my view, these are merely superficial reasons used by the uninformed to appear knowledgeable. The reality is that price clears all markets [and preference stacks]. What constitutes a good IPO at one price can be unfavorable at another. The financial system is flush with liquidity, and where there is capital, there is opportunity. I believe that more companies will follow Instacart's lead in going public at lower prices, making the issue an appealing buy.

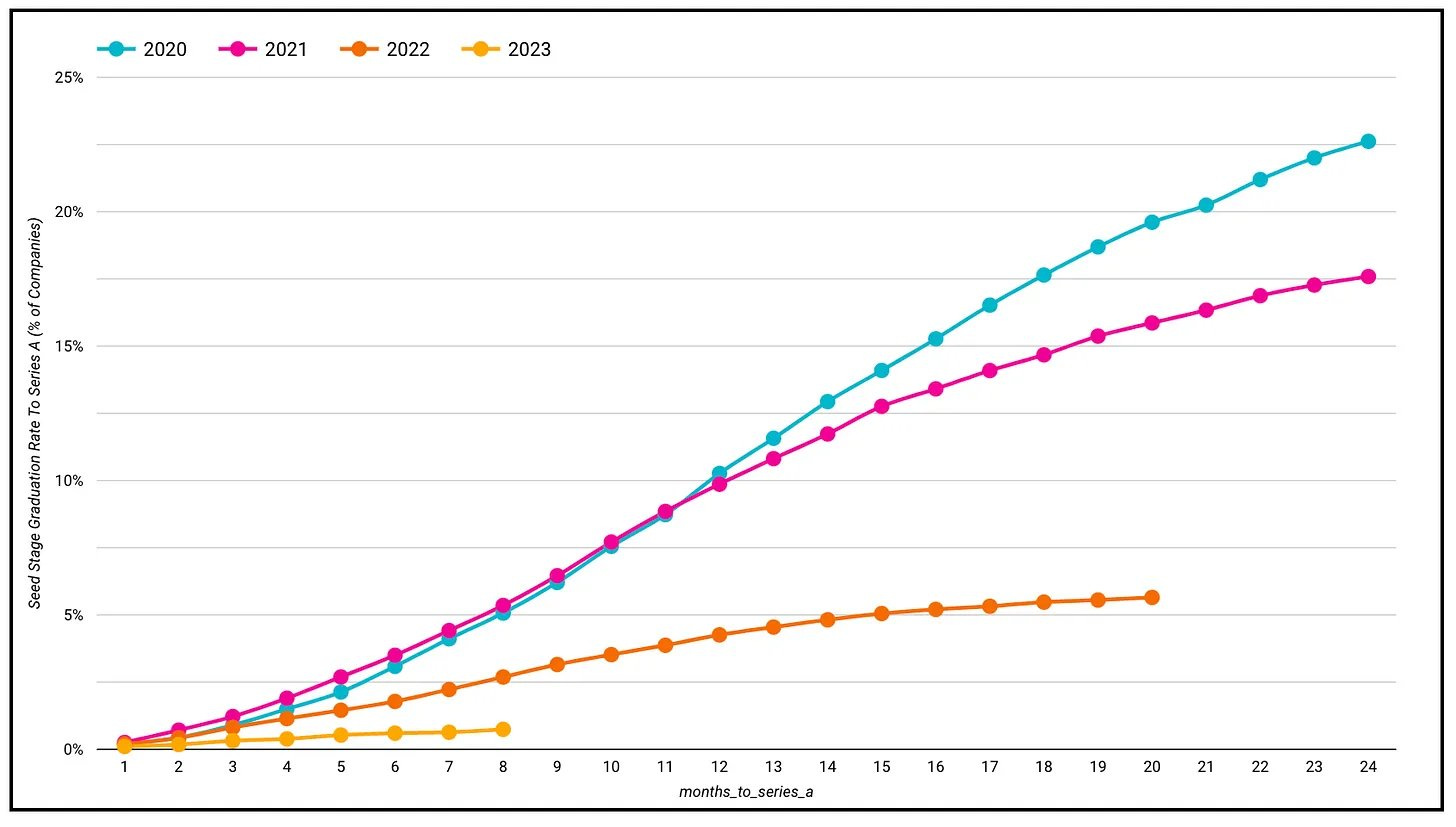

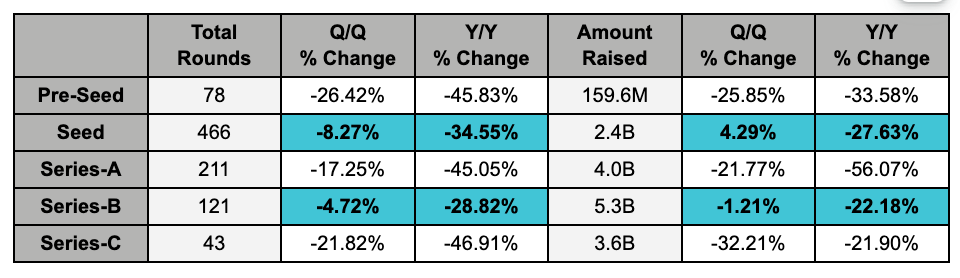

In the early-stage market, a particularly notable observation I have made is that the majority of our investments in 2023 have been predominantly in Seed rounds. This scarcity of Series A funding is a trend also observed by many of my peers. Unsurprisingly, the data shows a noticeable and industry-wide decline in the conversion rate from Seed to Series A investments since 2022.

Aggregate statistics bear out that Seed is the most resilient part of the market today.

In my opinion, the sobering reality behind the softness of the A+ VC market is straightforward: companies simply aren't performing well. As my tongue-in-cheek subtitle suggests, growth has been slow across many companies in the private markets, though there are certainly outliers. For example, I sit on the board of a company that is growing at 250% this year while generating nine figures in revenue. However, for most companies, the market for selling software has been sluggish throughout the year. The graph below illustrates growth challenges in the public markets.

The numbers provide some relief in Q3, but over the past year, growth in the software sector has faced challenges. The above chart, which measures the second derivative of public company ARR growth—specifically, Net ARR Added YoY—should always be positive if companies are growing exponentially. Anecdotally, in the private markets, I've observed that some companies are not experiencing any growth at all. Several factors could be contributing to this: strained corporate IT budgets, the rise of new tech incumbents with strong technology cultures, and the intense competition in the software market. Next month, Joe and I plan to explore this topic in more detail. Perhaps my most controversial viewpoint is that COVID-19, which spurred a 'great resignation' among high-performance collaborative cultures and a widespread shift to remote work, has slowed down nearly every company.

The unfortunate conclusion is that, with growth under pressure, I believe 2024 will surpass 2023 in terms of startup shutdowns, particularly among later-stage companies. We witnessed this trend in 2023, and it is likely to worsen in 2024:

The downside of the Venture Funding Markets is that many companies are struggling. However, the upside lies in the abundance of dry powder and the presence of numerous junior partners who are eager and ready to invest in great opportunities. The growth challenges we observe are not due to a lack of capital, as there is plenty available. If you identify a unique market opportunity, demonstrate strong capital efficiency metrics, and achieve solid benchmarks, you are in a good position to raise a substantial Series A round, which is likely to be competitive. We still see top performers out there. Companies not operating in saturated markets are performing well. If you aren’t in one of those markets, the key is to focus on managing burn rate. In my next update, I’ll discuss more about managing your company’s natural growth rate.

Lulls in growth are temporary and often pave the way for cyclical upswings. Don't lose hope or become overly focused on market updates — instead, strive to become an outlier!

Macro

The big news to end the quarter in the macroeconomic landscape appears to be 'The Fed Pivot' — indicating that the Federal Reserve has subtly signaled its intention to start cutting interest rates. In response, the market has obliged by pricing in six rate cuts for next year:

On the surface this makes some sense because we're seeing inflation ease, and based on money growth this should continue into 2024:

Up to Q3 2023, the money supply has been constricted through various means: Quantitative Tightening (QT—where the Fed shrinks the balance sheet), the Reverse Repo Facility (RRF, the Fed removing reserves from the banking system via repurchase agreements), and the build-up of the Treasury General Account (TGA, which also removes reserves from the banking system). These actions have contributed to a decline in M2. In Q4, with the exception of QT, these trends have started to reverse, primarily due to extreme deficits effectively injecting more liquidity into the system (drawing the RRF and TGA). The TLDR; is, much of what has led to M2 declines is starting to reverse, suggesting inflation pressure in 12+ months.

Beyond just monetary factors driving lower inflation, another element contributing to the decline is the recession occurring in the developed world outside of the US. This downturn is helping to suppress goods inflation, which has been a major factor in the overall reduction of inflation. However, this situation also poses a risk: cyclically, as the rest of the world begins to recover and grow in 2024, it could lead to renewed inflationary pressures. This is particularly concerning if it coincides with the Federal Reserve starting to ease its policies.

These coming inflation pressures (DM growth, RRP/TPA declining, strong US growth) coincide with massive, continued stimulatory government deficits, as illustrated below.

In summary, I believe that due to a confluence of factors, it is inevitable that inflation will resurface in late 2024 or early 2025. This is particularly likely given that core inflation currently stands at 3.9%, significantly higher than the target of 2%. The Federal Reserve's eventual decision to cut rates will likely be a mistake. Why would the Fed make such a mistake? It's primarily because inflation is expected to trend lower early in the year, coupled with a strong incentive to stimulate the economy ahead of the election.

In all likelihood, the Fed's easing in 2024 will present a favorable opportunity for founders to raise capital, as SaaS multiples will expand and liquidity will increase. However, I believe this situation will be short-lived. Therefore, 2024 is likely to offer a valuable, albeit brief, window for fundraising.

BioTech

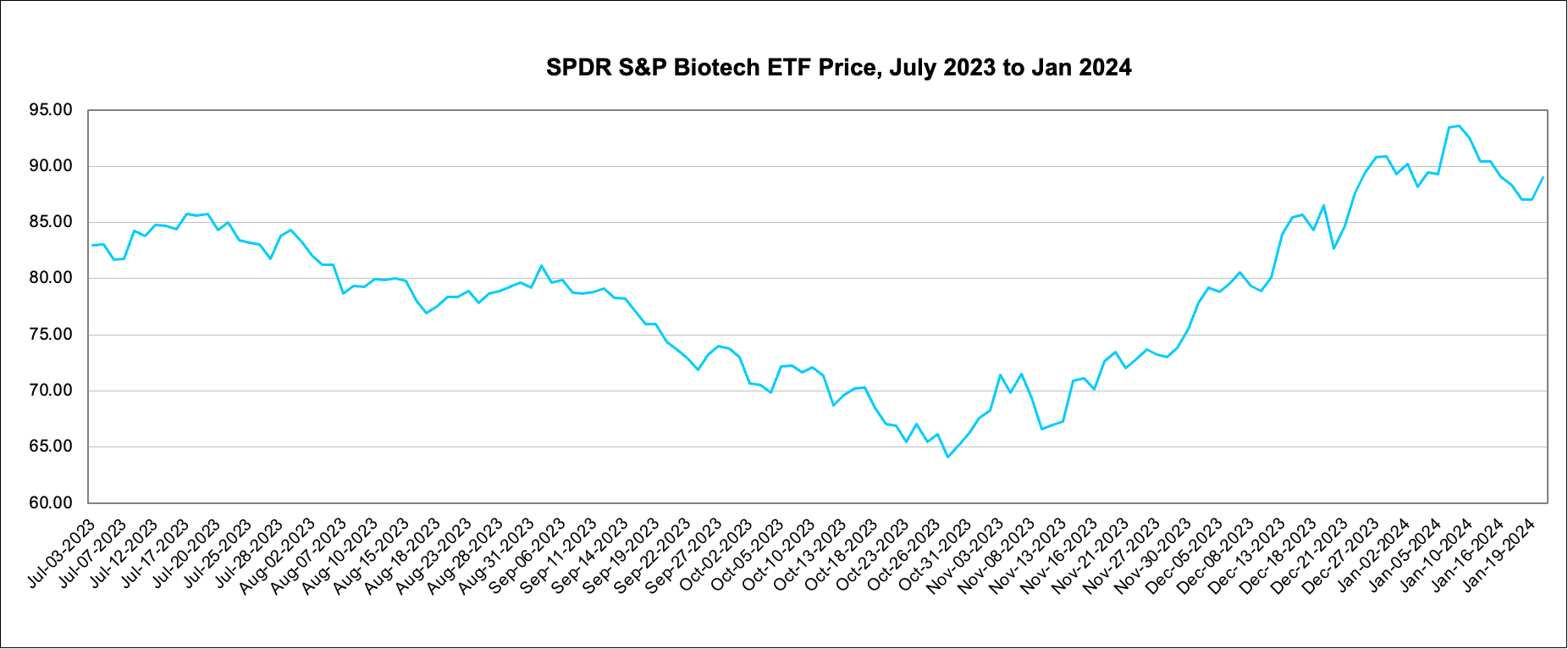

In this quarter, we observed notable activity in the public BioTech markets, particularly evident in the rally of the XBI. This rally was largely driven by M&A activity, with major deals such as the acquisitions of Karuna and Carmot standing out, valued at $14 billion and $2.7 billion, respectively. Year-over-year, M&A activity surged by 79%, totaling $152 billion, with $63 billion of that occurring in Q4 alone. This upward trend in M&A is likely to persist as Pharma companies aim to replenish their dwindling drug assets. An important factor in this trend is the $236 billion in Pharma revenue expected to come off patent between now and 2030, presenting a substantial liquidity tailwind for successful BioTech companies. On a personal note, I bought some XBI at the end of October — I’ll make sure to Tweet such investments in the future!

Even amidst the market rally and generally positive sentiment around M&A and partnerships, the BioTech sector remains subdued. As of EOY 2023, 169 public BioTech companies are trading at a negative Enterprise Value—they are worth less than cash. Put another way, many BioTech companies are so poorly valued that you can't give them away.

Sadly, I believe the private BioTech markets are in for a rough ride unless there's a significant increase in valuations, which, realistically, I don't anticipate happening. However, a challenging market does not necessarily mean a lack of investment opportunities. Often, it is during these rough times that the best investment opportunities arise — but realizing returns in such a market will be challenging.

Why do I believe there won't be a significant increase in valuations? As outlined in my Q3 note, I think we have entered what can be described as a new normal in valuation regimes, closely aligning with the environment before 2020. Notably, the XBI, although not my index of choice, is trading around the pre-2020 mean. This level, in my opinion, accurately reflects the current state of private market valuations as well. From my perspective, the valuations today, last seen in 2018, offer a more intrinsic representation of true therapeutic expected values, especially when compared to the inflated figures observed in 2020 and 2021.

Coming out of JPM, I’ve encountered a mix of positive and negative sentiments. On the positive side, Pharma companies continue to demonstrate a strong appetite for deals, either through partnerships or M&A. On the negative side, there are notable struggles in the private BioTech markets, with many companies quietly shutting down. This shutdown trend seems intuitive to me, and I anticipate witnessing even more shutdowns, regardless of whether valuations broadly increase.

Why do I think the private BioTech markets face major challenges? There are two primary reasons. Firstly, the excesses in the public BioTech markets during 2020 and 2021 led to a surge in the founding of weaker companies, leaving many private companies stranded. BioTech investing during this period resembled financial engineering more than traditional VC. The typical company-building strategy involved spinning out some interesting preclinical IP from a lab, assembling a credible management team, and then debuting it into the public markets at the preclinical stage — distribute to your investors, rinse, and repeat. I have always been skeptical of this model as an effective recipe for value creation. In my opinion, investors should commit to funding their companies through to clinical readouts while remaining private. Additionally, there had been considerable mimicry in target selection, which is likely to result in many inferior “me-too” assets of limited value. For example, ClinicalTrials.gov lists over 188 trials actively recruiting CD19-positive patients. Ironically, it’s the most crowded areas that are the riskiest and least value-accretive.

Secondly, many private BioTech companies are grappling with cost structures that don’t align with current market valuations. At our fund, I have been a vocal advocate for increasing our investment in BioTech, particularly in light of the recent decline in prices. However, we often encounter a significant challenge when considering investments at a company's proposed new post-money valuation (pre-money valuation + money in the round). Often, when comparing to similar companies, we find that the next funding round for these companies is likely to be flat or even down, despite them achieving significant milestones. Their burn rates are often expected to exceed the value they create.

Fundamentally, private BioTech companies need to improve their operational efficiency. It's common to see these companies recruiting numerous executives from Big Pharma, who often tend to establish a Pharma-like structure internally. This approach can lead to layered management and excessive staffing. In a startup environment, it is crucial for every team member to actively contribute. Additionally, significant advances in infrastructure have made therapeutic discovery more cost-effective. Companies should consider leveraging outsourced, cost-efficient platform discovery services, such as AlloyTX, to boost efficiency and reduce headcount. Such services can provide essential support while reducing overall burn.

Achieving high efficiency in the BioTech sector is indeed possible, especially in founder-driven companies. For instance, I have witnessed a BioTech company successfully advance a cell therapy to trials with just $40 million in funding. In another case, an antibody platform company efficiently delivered a Phase 1 asset with clinical readouts, supported its platform with only one partnership, and developed another IND-ready drug, all within a total budget of $60 million. Impressively, both companies have reported very positive outcomes from patient trials, suggesting capital expense is not always correlated to clinical efficacy.

Unfortunately, as the excess in the private BioTech markets is winding down, fundraising has become increasingly challenging. This is particularly true for early-stage funding, where most investors are now focused on supporting their existing portfolio companies through flat or bridge funding rounds, rather than exploring new opportunities. For example, we are closely involved with two companies that have been trying for 12 months to secure their Series A funding round, illustrating the heightened difficulties in the current investment climate.

The fundraising situation in the BioTech sector is unlikely to see immediate improvement, particularly in light of the potential shutdown of BioTech VC firms who were active in the recent 2020 investment frenzy. This could further deplete an already limited capital pool. Despite these challenges, I am hopeful for two positive developments: Firstly, a broader realization within the BioTech market that capital is not unlimited, which could prompt a reset in cost structures. Secondly, the closure of unviable companies may allow valuable talent to reenter and enrich the ecosystem.

In the midst of the prevailing doom and gloom, I remain steadfastly optimistic about lean BioTech companies that are adept at navigating the current environment. A significant benefit of the ZIRP era was the discovery of numerous ‘0-1’ innovations, spurred by the funding available during that period. Once translated, these innovations are likely to produce many groundbreaking clinical drugs. The next generation of BioTech companies, built upon this wave of innovation and focusing on cost-effective scaling, are well-positioned to capitalize on this investment. Moreover, the impending patent cliff in Big Pharma — with an estimated $236 billion in revenue expected to come off patent by 2030 — presents a substantial opportunity for companies that can demonstrate clinical proof of concept. Entrepreneurs and investors who are efficient in developing and delivering effective drugs are likely to find an abundance of capital for exits.

AI

Wow, this note is much longer than I had hoped, and we're just starting to discuss AI. I have a feeling that AI will be a frequent topic in these writings. The first thing I'll cover is what type of disruptive technology I believe AI represents.

Let me set the expectations upfront: I'm e/acc and I'm a believer. I wasn’t among the earliest to recognize the potential of Transformer Architectures, but using ChatGPT in December 2022 was a groundbreaking experience for me—the first time a new technology truly awed me. Having studied AI/ML extensively in the 2000s and early 2010s, I initially believed it would be valuable but not necessarily revolutionary. Now, I am convinced that Large Language Models (LLMs) will drive fundamental change in our society. In my opinion, we are on the cusp of the next industrial revolution, driven by AI. I anticipate that AI will be over-hyped in the short term (1-3 years), a period likely marked by struggles in AI infrastructure companies and disappointments in AI deployment, which I call the '90/10 problem.' But looking ahead, I believe that in the next decade, AI will dramatically transform a significant portion of knowledge work.

What changes do I foresee with the advancement of AI? Here are some key shifts that come to mind:

The landscape of commercial go-to-market strategies will undergo a radical transformation. As a buyer you'll get an overwhelming number of perfectly personalized AI-generated emails and phone calls. As a result, buyers will likely start to rely more on referrals, in-person tradeshows, and trade associations for trustworthy product recommendation

Professions that primarily involve synthesizing mostly structured knowledge are set to diminish. This includes careers like programming, law, consulting, and certain medical practices, which will gradually become less prevalent.

A key area of human defensibility will be in aiding human interactions with AI in complex or emotionally charged situations. For example, the lawyers who adapt will focus on gathering context to feed into AI lawyers. Similarly, Doctors will work with patients to gather context and explain complex or emotional realities

So far, LLMs have primarily targeted digital and knowledge-based domains. Disruption in physical labor by AI, with pre trained Robotic Transformer Models, is likely further down the line (I am currently exploring this area and would welcome introductions to anyone working on it).

Ironically, those who told coal miners to learn to code, will be the ones out of a job before the miners themselves; both journalists and programmers!

I often wonder what the future will look like in 50 years, once LLMs have fully integrated into our lives and automated knowledge-work. The somewhat ironic Marxist perspective suggests that we may shift towards more community-oriented living, as most of the remaining work will be on a human scale. If you visit a village in southern Italy, you'll notice that most activities there would remain largely unchanged in a post-LLM world. I believe our future might more closely resemble this kind of lifestyle.

Now, let's address the questions: Are LLMs a platform? And do they represent a sustaining or disruptive innovation?

The first answer depends on your definition of a software platform. If we consider whether new software systems will be built on top of LLMs as their underlying hosted platform of record, technical framework, or UI, then the answer is probably no. For the foreseeable future, I believe LLMs will primarily serve as additive features/services to software systems built on existing platforms. Even once Artificial General Intelligence (AGI) is achieved, the AGI system itself will likely become the ultimate core system of record. This is because it would be all-knowing and capable of building any supplemental infrastructure it may need, rather than serving as the foundational layer upon which a software system is structured.

I believe that LLMs offer a significant advantage to software vendors who already have an established customer base. Consider a scenario where you operate a title insurance franchise and wish to automate much of your document processing using LLMs. In this case, it's more likely that you would opt for AI features from your existing System of Record (SOR) vendor, assuming they have integrated such capabilities, rather than acquiring a completely new system built from scratch to incorporate LLMs. The primary reason for this belief is the inherent ease of integrating LLMs. By inputting the right context and the appropriate prompt in English, a developer can tap into most of the capabilities that the LLM offers for a specific workflow. This suggests that even legacy players in the industry should find success in integrating these technologies.

As to whether LLMs are disruptive or sustaining innovations, I believe the answer depends on the market in question, given their broad applicability.

For enterprise Independent Software Vendors (ISVs), as discussed LLMs are currently a sustaining innovation.

For some consumer internet companies, like Google, whose products rely on interpreting, synthesizing, or reasoning based on public knowledge, they are disruptive innovations. LLMs are a step-function improvement but at a much higher (real) price-point. (Perplexity.ai is a way better product than Google but more costly to run a query). If costs come down, then existing consumer franchises can be threatened (i.e. where there is less of an install-base lock-in and more a brand-effect).

For white-collar workers, AI represents a disruptive technology. At present, LLMs primarily compete in tasks of lower quality and with limited reliability. However, over time, they are likely to disrupt many aspects of the work performed by knowledge workers, as previously described.

In the very long term, there's a possibility that LLMs could disrupt enterprise ISVs. If LLMs evolve to translate requirements into fully-fledged systems (including migration scripts), then every software sale might face competition from a (less expensive) custom build via an LLM. This scenario would massively disrupt enterprise software pricing. However, my reservation lies in three counter-arguments: a) as Steve Jobs pointed out, there's always room for taste in products, b) ISVs offer more services than just software, and c) most customers don't quite know how to describe what they want. If we harken back to the old-days of Software Engineering in the 80s/90s, half of all internal software projects would fail. A large part of that was due to requirements gathering and design being a real challenge -- not implementation!

So, there's a lot of theory, but where are the opportunities? I believe that the first-order effects of AI are already priced in—when looking at foundation models, consumer products, or certain types of AI infrastructure, there is no alpha. [As an aside, AI is probably one of the few areas where alpha was priced out even when it was somewhat contrarian, as many hot companies had seed rounds at valuations of $100m+ pre-money].

In my opinion, the second-order effects are where the opportunities lie. In no particular order and non-exhaustively:

AI-enabled services - This is probably the area I'm most bullish on at the moment. Consider existing businesses that provide a service; augment labor as much as possible with AI, and quickly dominate the space with that cost advantage. Key areas are ones which include structured information extraction, summarization, knowledge retrieval, and basic document synthesis tasks.

Net-new application layer products (voice, enterprise search, etc...) - As mentioned above, I'm not a proponent of rewriting the existing application layer. However, new application spaces are now feasible with AI. The bar is high; one must ask, 'Does AI fundamentally enable this new product?' Interesting areas include those with unstructured input data, different input modalities (voice, music, images), or where there is inherent bundling of multiple products because LLMs make it easier to integrate workflows together (from prospecting to sales outreach).

Serverless training/burst GPU computing - Anecdotally, we hear of very low utilization rates for prepaid GPU resources, as low as 10% in major data centers. This inefficiency seems ripe for a solution.

Open Source - I am a strong advocate of Open Source models (more on this in the next update). Consequently, tooling for deploying, tuning, etc., to make these models more accessible will be highly valuable.

LLM Evaluation/monitoring/production readiness - Suppose I've developed an LLM application and want to deploy it. Key considerations include: a) evaluating the boundary conditions my model will work within, b) understanding the error rate, c) testing and d) determining if a new foundational model is disrupting my application (i.e., how to test subjective outputs).

Enterprise LLM application development tooling - Similar to the above, the tooling for creating LLM applications needs enhancement. Enterprises need comprehensive solutions for creating a RAG-stack that respects permissions, chunks data properly, optimizes embeddings, distills a model, and even provides guidance on how to effectively prompt a model, especially one that has been fine-tuned, to achieve the best results.

Code generation: Coding is likely to be one of the first areas significantly enhanced by AI. There will be room for a variety of tools aimed at boosting internal developer productivity, especially in environments where code security is of paramount importance.

Conclusion to 2024

This update ended up being much longer than I had thought. Whenever I look forward to 2024, I find myself thinking things will be extremely turbulent but optimistic. The natural conclusion of poor startup growth is that 2024 will see more startups go bust than ever (inVision which raised $350m at $2b valuation just died). At the same time, an easing Fed will likely present an opportunity for growing startups to raise money on favorable terms (in public or private market). There will be haves and have nots.

With the upcoming turmoil facing under-performing businesses, I am optimistic about witnessing a cultural and cathartic rebirth that Silicon Valley urgently needs. In my view, COVID-19 brought about a 'Great Resignation' in the commitment of employees to high-performance, collaborative company cultures. This change saw many startup employees lose their deep connection with their work. The Great Resignation has been one of the most destructive yet least discussed trends in the startup economy. I anticipate that, with companies under stress, there will be an end to this period of decadence. And that insane, collaborative, optimistic spark which makes Silicon Valley tick will come back again.

Interesting things to read/watch:

Founding of Transdigm:

Karpathy intro to LLMs:

History of Nvidia on the Acquired Podcast:

Grindset is a great term for this market. What do you think of EdTech? Like healthcare, COVID exposed that the education system is broken and needs innovation to support the builders of tomorrow.

Thanks for sharing - Will be interesting to see how 2024 shakes out for SaaS as we start to see the results of AI-driven product upgrades/implementations in some of the larger players (ie. ServiceNow), how do you think this will disrupt 'newer entrants' and companies 'in the middle'?